1

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

For the quarterly period ended

OR

For the transition period from to

Commission File Number:

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation) | (IRS Employer Identification Number) | |

| ||

(Address of principal executive offices) (Zip Code) | ||

( | ||

(Registrant’s telephone number, including area code) N/A (Former Name, Former Address and Former Fiscal Year, | ||

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

| Trading Symbol(s) |

| Name of each exchange on which registered |

|

| The |

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐ | Accelerated filer ☐ |

Smaller reporting company | |

Emerging growth company |

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

As of February 5, 2024, the registrant had

TABLE OF CONTENTS

2 | ||

2 | ||

Management’s Discussion and Analysis of Financial Condition and Results of Operations. | 29 | |

50 | ||

50 | ||

51 | ||

51 | ||

51 | ||

Unregistered Sales of Equity Securities and Use of Proceeds. | 52 | |

52 | ||

52 | ||

52 | ||

52 | ||

54 | ||

PART I — FINANCIAL INFORMATION

Item 1.Financial Statements.

LOOP MEDIA, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

December 31, |

| September 30, | |||

2023 | 2023 | ||||

ASSETS | (UNAUDITED) |

|

| ||

Current assets |

|

|

| ||

Cash | $ | | $ | | |

Accounts receivable, net |

| |

| | |

Prepaid expenses and other current assets |

| |

| | |

Content assets - current | | | |||

Total current assets |

| |

| | |

Non-current assets |

|

|

|

| |

Deposits |

| |

| | |

Content assets - non current | | | |||

Deferred costs - non current | | | |||

Property and equipment, net |

| |

| | |

Intangible assets, net |

| |

| | |

Total non-current assets |

| |

| | |

Total assets | $ | | $ | | |

LIABILITIES AND STOCKHOLDERS’ EQUITY (DEFICIT) |

|

|

| ||

Current liabilities |

|

|

|

| |

Accounts payable | $ | | $ | | |

Accrued liabilities | | | |||

Accrued royalties and revenue share | | | |||

License content liabilities - current | | | |||

Deferred Income |

| |

| — | |

Revolving line of credit, current | | | |||

Non-revolving line of credit |

| |

| | |

Total current liabilities |

| |

| | |

Non-current liabilities |

|

|

|

| |

License content liabilities - non current | | | |||

Non-revolving line of credit |

| |

| | |

Non-revolving line of credit, related party | — | | |||

Total non-current liabilities |

| |

| | |

Total liabilities |

| |

| | |

Commitments and contingencies (Note 9) | |||||

Stockholders’ equity (deficit) | |||||

Common Stock, $ |

| | | ||

Additional paid in capital |

| | | ||

Accumulated deficit |

| ( | ( | ||

Total stockholders' equity (deficit) |

| ( |

| ( | |

Total liabilities and stockholders' equity (deficit) | $ | | $ | | |

See the accompanying notes to the consolidated financial statements

2

LOOP MEDIA, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(UNAUDITED)

Three months ended December 31, | ||||||

| 2023 | 2022 | ||||

Revenue | $ | | $ | | ||

Cost of revenue |

| |||||

Cost of revenue - Advertising and Legacy and other revenue | | | ||||

Cost of revenue - depreciation and amortization | | | ||||

Total cost of revenue | | | ||||

Gross profit | |

| | |||

Operating expenses |

|

|

| |||

Sales, general and administrative | |

| | |||

Stock-based compensation | | | ||||

Depreciation and amortization | | | ||||

Total operating expenses | |

| | |||

Loss from operations | ( |

| ( | |||

Other income (expense) |

|

|

| |||

Interest income |

| — | ||||

Interest expense | ( |

| ( | |||

Loss on extinguishment of debt | ( |

| — | |||

Other expense | ( | — | ||||

Total other income (expense) | ( |

| ( | |||

Loss before income taxes | ( | ( | ||||

Income tax (expense)/benefit | — |

| ( | |||

Net loss | $ | ( | $ | ( | ||

Basic and diluted net loss per common share (Note 2) | $ | ( | $ | ( | ||

Weighted average number of basic and diluted common shares outstanding | |

| | |||

See the accompanying notes to the consolidated financial statements

3

LOOP MEDIA, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENT OF CHANGES IN STOCKHOLDERS’ EQUITY

FOR THE THREE MONTHS ENDED DECEMBER 31, 2023, and 2022

(UNAUDITED)

Common Stock | Additional Paid | Accumulated | ||||||||||||

Shares | Amount | in Capital | Deficit | Total | ||||||||||

Balances, September 30, 2023 |

| |

| $ | |

| $ | |

| $ | ( |

| $ | ( |

Stock-based compensation | | | ||||||||||||

Warrants issued for debt | | | ||||||||||||

Warrants issued for consulting fees | | | ||||||||||||

Shares issued for consulting fees | | | | | ||||||||||

Shares issued for debt conversion | | | | | ||||||||||

Shares issued for capital raise costs | | | | | ||||||||||

Shares issued upon warrant exercises | | | | | ||||||||||

Net loss |

| — |

| — |

| — |

| ( |

| ( | ||||

Balances, December 31, 2023 |

| | $ | | $ | | $ | ( | $ | ( | ||||

Common Stock | Additional Paid | Accumulated | ||||||||||||

Shares | Amount | in Capital | Deficit | Total | ||||||||||

Balances, September 30, 2022 |

| |

| $ | |

| $ | |

| $ | ( |

| $ | |

Stock-based compensation | — | — | | — | | |||||||||

Net loss |

| — |

| — |

| — |

| ( |

| ( | ||||

Balances, December 31, 2022 |

| | $ | | $ | | $ | ( | $ | | ||||

See the accompanying notes to the consolidated financial statements

4

LOOP MEDIA, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(UNAUDITED)

Three months ended December 31, | |||||

2023 |

| 2022 | |||

CASH FLOWS FROM OPERATING ACTIVITIES |

|

|

| ||

Net loss | $ | ( | $ | ( | |

Adjustments to reconcile net loss to net cash used in operating activities: |

|

|

| ||

Amortization of debt discount |

| | | ||

Depreciation and amortization expense |

| | | ||

Amortization of content assets | | | |||

Amortization of right-of-use assets |

| — | | ||

Bad debt expense | | — | |||

Extinguishment of debt converted to equity | | — | |||

Loss on extinguishment of debt converted to equity | | — | |||

Stock-based compensation |

| | | ||

Shares issued for capital raise costs | | — | |||

Shares issued for consulting fees | | — | |||

Change in operating assets and liabilities: |

|

| |||

Accounts receivable |

| ( | ( | ||

Inventory |

| ( | | ||

Prepaid expenses |

| | | ||

Deposit |

| ( | — | ||

Accounts payable |

| | ( | ||

Accrued liabilities | ( | ( | |||

Accrued royalties and revenue share | | | |||

License content liability |

| ( | ( | ||

Operating lease liabilities |

| — | ( | ||

Deferred income |

| | | ||

NET CASH USED IN OPERATING ACTIVITIES |

| ( |

| ( | |

CASH FLOWS FROM INVESTING ACTIVITIES |

|

|

|

| |

Purchase of property and equipment |

| ( | ( | ||

NET CASH USED IN INVESTING ACTIVITIES |

| ( |

| ( | |

CASH FLOWS FROM FINANCING ACTIVITIES |

|

|

|

| |

Proceeds from lines of credit | | | |||

Repayments on lines of credit | ( | ( | |||

Proceeds from exercise of warrants | | — | |||

Deferred costs | ( | ( | |||

Payment of acquisition related consideration | — | ( | |||

Debt issuance costs | — | ( | |||

NET CASH PROVIDED BY FINANCING ACTIVITIES |

| |

| | |

Change in cash and cash equivalents |

| |

| ( | |

Cash, beginning of period |

| |

| | |

Cash, end of period | $ | | $ | | |

SUPPLEMENTAL DISCLOSURES OF CASH FLOW STATEMENTS |

|

|

|

| |

Cash paid for interest | $ | | $ | | |

Cash paid for income taxes | $ | — | $ | | |

SUPPLEMENTAL DISCLOSURES OF NON CASH INVESTING AND FINANCING ACTIVITIES |

|

|

|

| |

Shares issued for debt conversion | $ | | $ | — | |

Deferred costs for warrants issued for debt | $ | | $ | — | |

Unpaid additions to licensed content and internally developed content | $ | | $ | | |

Unpaid deferred costs | $ | | $ | | |

Unpaid additions to property and equipment | $ | | $ | | |

See the accompanying notes to the consolidated financial statements

5

LOOP MEDIA, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2023

(UNAUDITED)

NOTE 1 – BUSINESS

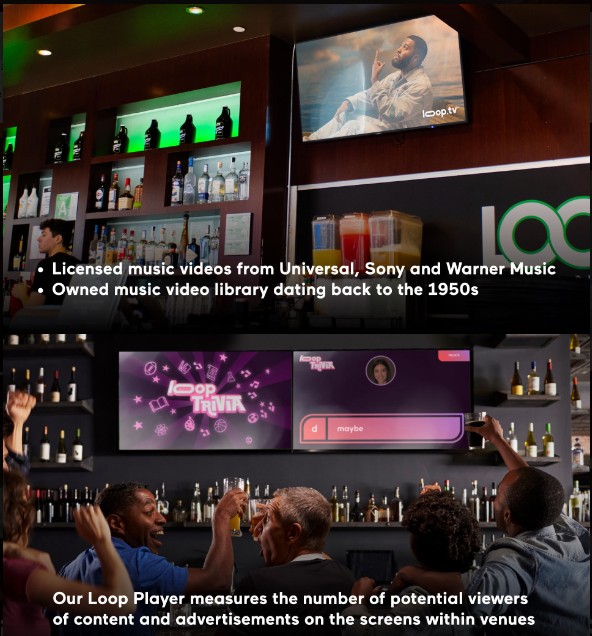

Loop Media, Inc., a Nevada corporation, (collectively, “Loop Media,” the “Company,” “we,” “us” or “our”) is a multichannel digital video platform media company that uses marketing technology, or “MarTech,” to generate our revenue and offer our services. Our technology and vast library of videos and licensed content enable us to curate and distribute short-form videos to connected televisions (“CTV”) in out-of-home (“OOH”) dining, hospitality and retail establishments, convenience stores and other locations and venues to enable them to inform, entertain and engage their customers. Our technology also provides businesses the ability to promote and advertise their products via digital signage and provides third-party advertisers with a targeted marketing and promotional tool for their products and services. We also allow our business clients to access our service without advertisements by paying a monthly subscription fee.

We offer hand-curated music video content licensed from major and independent record labels, including Universal Music Group (“Universal”), Sony Music Entertainment (“Sony”), and Warner Music Group (“Warner” and collectively with Universal and Sony, the “Music Labels”), as well as non-music video content. Our non-music video content is predominantly licensed or acquired from third parties, including action sports clips, drone and nature footage, trivia, news headlines, lifestyle channels and kid-friendly videos, as well as movie, television and video game trailers, amongst other content. We distribute our content and advertising inventory to digital screens located in OOH locations primarily through (i) our owned and operated platform (the “O&O Platform”) of Loop Media-designed “small-box” streaming Android media players (“Loop Players”) and legacy ScreenPlay (as defined below) computers and (ii) through screens (“Partner Screens”) on digital platforms owned and operated by third parties (each a “Partner Platform” and collectively, the “Partner Platforms,” and together with the O&O Platform, the “Loop Platform”).

As of December 31, 2023, we had approximately

Liquidity and management’s plan

As shown in the accompanying consolidated financial statements, we have incurred significant recurring losses resulting in an accumulated deficit. We anticipate further losses in the foreseeable future. We also had negative cash flows used in operations. These factors raise substantial doubt about our ability to continue as a going concern.

On December 22, 2022, we filed a Shelf Registration Statement on Form S-3 that has been declared effective by the Securities and Exchange Commission (“SEC”). On May 12, 2023, we entered into an At Market Issuance Sales Agreement (the “ATM Sales Agreement”) with B. Riley Securities, Inc. (the “Agent”) pursuant to which we may offer and sell, from time to time through the Agent, shares of our common stock, par value $

6

time to time. We have not raised any funds through sales under our ATM Sales Agreement from January 1, 2024, through the date of this Report.

Effective as of December 14, 2023, we entered into a Revolving Line of Credit Loan Agreement with Excel Family Partners, LLLP (“Excel” and the “Excel Revolving Line of Credit Agreement”) for up to a principal sum of $

Based on the available cash balance at December 31, 2023, and our current access to capital utilizing the ATM and our credit facilities, we believe that we will have sufficient resources to fund our operations for at least twelve months from the date these financial statements were issued and that the substantial doubt in connection with our ability to continue as a going concern is alleviated.

NOTE 2 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Interim Financial Statements

The following (a) condensed consolidated balance sheet as of September 30, 2023, which has been derived from our audited financial statements, and (b) our unaudited condensed consolidated interim financial statements for the three months ended December 31, 2023, have been prepared in accordance with accounting principles generally accepted in the United States ("US GAAP") for interim financial information and the instructions to Form 10-Q and Rule 8-03 of Regulation S-X of the Securities Act of 1933. Accordingly, they do not include all of the information and footnotes required by US GAAP for complete financial statements. In the opinion of management, all adjustments (consisting of normal recurring accruals) considered necessary for a fair presentation have been included. Operating results for the three months ended December 31, 2023, are not necessarily indicative of results that may be expected for the year ending September 30, 2024.

These unaudited condensed consolidated financial statements should be read in conjunction with the audited consolidated financial statements and notes thereto for the year ended September 30, 2023, included in our Annual Report on Form 10-K filed with the SEC on December 19, 2023.

Basis of presentation

The consolidated financial statements include our accounts and our wholly-owned subsidiaries, EON Media Group Pte. Ltd. and Retail Media TV, Inc. The unaudited condensed consolidated financial statements are prepared using the accrual basis of accounting in accordance with US GAAP. All inter-company transactions and balances have been eliminated on consolidation.

Use of estimates

The preparation of the unaudited condensed consolidated financial statements in conformity with US GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the reporting period. Actual results could differ from those estimates. Significant estimates include assumptions used in the revenue recognition of performance obligations, allowance for doubtful accounts, fair value of stock-based compensation awards, income taxes and going concern.

Segment reporting

We report as

7

In November 2023, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) 2023-07, Segment Reporting (Topic 280): Improvements to Reportable Segment Disclosures, that would enhance disclosures for significant segment expenses for all public entities required to report segment information in accordance with ASC 280. ASC 280 requires a public entity to report for each reportable segment a measure of segment profit or loss that its chief operating decision maker (“CODM”) uses to assess segment performance and to make decisions about resource allocations. The amendments in ASU 2023-07 improve financial reporting by requiring disclosure of incremental segment information on an annual and interim basis for all public entities to enable investors to develop more useful financial analyses. Currently, Topic 280 requires that a public entity disclose certain information about its reportable segments. For example, a public entity is required to report a measure of segment profit or loss that the CODM uses to assess segment performance and make decisions about allocating resources. ASC 280 also requires other specified segment items and amounts such as depreciation, amortization and depletion expense to be disclosed under certain circumstances. The amendments in ASU 2023-07 do not change or remove those disclosure requirements. The amendments in ASU 2023-07 also do not change how a public entity identifies its operating segments, aggregates those operating segments, or applies the quantitative thresholds to determine its reportable segments. The amendments in ASU 2023-07 are effective for fiscal years beginning after December 15, 2023, and interim periods within fiscal years beginning after December 15, 2024. Early adoption is permitted. A public entity should apply the amendments in ASU 2023-07 retrospectively to all prior periods presented in the financial statements. We are currently evaluating the impact of this standard on our condensed consolidated financial statements and related disclosures.

Cash

Cash and cash equivalents include all highly liquid monetary instruments with original maturities of three months or less when purchased. These investments are carried at cost, which approximates fair value. Financial instruments that potentially subject us to concentrations of credit risk consist primarily of cash deposits. We maintain our cash in institutions insured by the Federal Deposit Insurance Corporation (“FDIC”). At times, our cash and cash equivalent balances may be uninsured or in amounts that exceed the FDIC insurance limits. We have not experienced any losses on such accounts. On December 31, 2023, and September 30, 2023, we had

As of December 31, 2023, and September 30, 2023, approximately $

Accounts receivable

Accounts receivable represent amounts due from customers. We assess the collectability of receivables on an ongoing basis. A provision for the impairment of receivables involves significant management judgment and includes the review of individual receivables based on individual customers, current economic trends and analysis of historical bad debts. As of December 31, 2023, and September 30, 2023, we had recorded an allowance for doubtful accounts of $

Concentration of credit risk

During the three months ended December 31, 2023, we had

During the three months ended December 31, 2022, we had

As of December 31, 2023,

As of December 31, 2022,

8

We grant credit in the normal course of business to our customers. Periodically, we review past due accounts and make decisions about future credit on a customer-by-customer basis. Credit risk is the risk that one party to a financial instrument will cause a loss for the other party by failing to discharge an obligation.

Prepaid expenses

Expenditures paid in one accounting period which will not be consumed until a future period such as insurance premiums and annual subscription fees are accounted for on the balance sheet as a prepaid expense. When the asset is eventually consumed, it is charged to expense.

Content Assets

We capitalize the fixed content fees and corresponding liability when the license period begins, the cost of the content is known, and the content is accepted and available for streaming. If the licensing fee is not determinable or reasonably estimable, no asset or liability is recorded, and licensing costs are expensed as incurred. We amortize licensed content assets into cost of revenue, using the straight-line method over the contractual period of availability. The liability is paid in accordance with the contractual terms of the arrangement. Internally-developed content costs are capitalized in the same manner as licensed content costs, when the cost of the content is known and the content is ready and available for streaming. We amortize internally-developed content assets into cost of revenue, using the straight-line method over the estimated period of streaming.

Long-lived assets

We evaluate the recoverability of long-lived assets, including intangible assets, for impairment when events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. Conditions that would necessitate an impairment assessment include a significant decline in the observable market value of an asset, a significant change in the extent or manner that an asset is used, or a significant adverse change that would indicate that the carrying amount of an asset or group of assets is not recoverable. For long-lived assets to be held and used, we recognize an impairment loss only if their carrying amount is not recoverable through the undiscounted cash flows. The impairment loss is based on the difference between the carrying amount and estimated fair value as determined by discounted future cash flows. Our finite long-lived intangible assets are amortized on a straight-line basis over their estimated useful lives, which range from to .

Property and equipment, net

Property and equipment are stated at cost, less accumulated depreciation. Depreciation is calculated using the straight-line method over the asset’s estimated useful life. Our capitalization policy is to capitalize property and equipment purchases greater than $

Loop Players are capitalized as fixed assets and depreciated over the estimated period of use.

See below for estimated useful lives:

Loop Players | ||

Equipment |

| |

Software |

Operating leases

We determine if an arrangement is a lease at inception. Operating lease right-of-use assets (“ROU assets”) and short-term and long-term lease liabilities are included on the face of the consolidated balance sheet.

9

ROU assets represent the right to use an underlying asset for the lease term and lease liabilities represent our obligation to make lease payments arising from the lease. Operating lease ROU assets and liabilities are recognized at commencement date based on the present value of lease payments over the lease term. As most of our leases do not provide an implicit rate, we use an incremental borrowing rate based on the information available at commencement date in determining the present value of lease payments. Our lease terms may include options to extend or terminate the lease when it is reasonably certain that we will exercise that option. Lease expense for lease payments is recognized on a straight-line basis over the lease term. We have lease agreements with lease and non-lease components, which are accounted for as a single lease component. For lease agreements with terms less than twelve months, we have elected the short-term lease measurement and recognition exemption, and we recognize such lease payments on a straight-line basis over the lease term.

Fair value measurement

We determine the fair value of our assets and liabilities using a hierarchy established by the accounting guidance that prioritizes the inputs to valuation techniques used to measure fair value. The hierarchy gives the highest priority to valuations based upon unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to valuations based upon unobservable inputs that are significant to the valuation (Level 3 measurements). The three levels of valuation hierarchy are defined as follows:

| ● | Level 1 inputs to the valuation methodology are quoted prices for identical assets or liabilities in active markets. |

| ● | Level 2 inputs to the valuation methodology included quoted prices for similar assets and liabilities in active markets, quoted prices for identical or similar assets in inactive markets, and inputs that are observable for the asset or liability, either directly or indirectly, for substantially the full term of the financial instrument. |

| ● | Level 3 inputs to the valuation methodology is one or more unobservable inputs which are significant to the fair value measurement. |

The carrying amount of our financial instruments, including cash, accounts receivable, deposits, short-term portion of notes receivable and notes payable, and current liabilities approximate fair value due to their short-term nature. We do not have financial assets or liabilities that are required under US GAAP to be measured at fair value on a recurring basis. We have not elected to use fair value measurement option for any assets or liabilities for which fair value measurement is not presently required.

We record assets and liabilities at fair value on a nonrecurring basis as required by US GAAP. Assets recognized or disclosed at fair value in the condensed consolidated financial statements on a nonrecurring basis include items such as property and equipment, operating lease assets, goodwill, and other intangible assets, which are measured at fair value if determined to be impaired.

On September 26, 2022, our convertible debentures converted to Common Stock as part of our public offering and uplist to The NYSE American, LLC, in accordance with the terms of the original debt agreements. As of September 30, 2022, the remaining balance of the Derivative Liability was written off as part of the conversion to equity. Thus, there is

Advertising costs

We expense all advertising costs as incurred. Advertising and marketing costs for the three months ended December 31, 2023, and 2022, were $

Revenue recognition

We recognize revenue in accordance with ASC 606, Revenue from Contracts with Customers, when it satisfies a performance obligation by transferring control over a product to a customer. Revenue is measured based on the

10

consideration we expect to receive in exchange for those products. In instances where final acceptance of the product is specified by the client, revenue is deferred until all acceptance criteria have been met. For example, we bill subscription services in advance of when the service is performed and revenue is treated as deferred revenue until the service is performed and/or the performance obligation is satisfied. Revenues are recognized under Topic 606 in a manner that reasonably reflects the delivery of our products and services to clients in return for expected consideration and includes the following elements:

| ● | executed contracts with our customers that we believe are legally enforceable; |

| ● | identification of performance obligations in the respective contract; |

| ● | determination of the transaction price for each performance obligation in the respective contract; |

| ● | allocation of the transaction price to each performance obligation; and |

| ● | recognition of revenue only when we satisfy each performance obligation. |

Our revenue can be categorized into two revenue streams: Advertising revenue and Legacy and other revenue.

The following table disaggregates our revenue by major type for each of the periods indicated:

Three months ended December 31, | ||||||

2023 | 2022 | |||||

Advertising revenue | $ | | $ | | ||

Legacy and other revenue | | | ||||

Total | $ | | $ | | ||

Performance obligations and significant judgments

Our performance obligations and recognition patterns for each revenue stream are as follows:

Advertising revenue

For the three months ended December 31, 2023, and 2022, advertising revenue accounts for

For all advertising revenue sources, we evaluate whether we should be considered the principal (i.e., report revenues on a gross basis) or an agent (i.e., report revenues on a net basis). Our role as principal or agent differs based on our performance obligation for each revenue share arrangement.

For both the O&O and Partner Platforms businesses, advertising inventory provided to advertisers through the use of an advertising demand partner or agency, with whose fees or commission is calculated based on a stated percentage of gross advertising spending, we are considered the agent and our revenues are reported net of agency fees and commissions. We are considered the agent because the demand partner or agency controls all aspects of the transaction (pricing risk, inventory risk, obligation for fulfillment) except for the devices used to show the advertisements, therefore we report this advertising revenue net of agency fees and commissions.

11

We are considered the principal in our arrangements with content providers in our O&O Platform business and with our arrangements with our third-party partners in our Partner Platforms business and thus report revenues on a gross basis (net of agency fees and commissions), wherein the amounts billed to our advertising demand partners, advertising agencies, and direct advertisers and sponsors are recorded as revenues, and amounts paid to content providers and third-party partners are recorded as expenses. We are considered the principal because we control the advertising space, are primarily responsible to our advertising demand partners and other parties filling our advertising inventory, have discretion in pricing and advertising fill rates and typically have an inventory risk.

For advertising revenue, we recognize revenue at the time the digital advertising impressions are filled and the advertisements are played and, for sponsorship revenue, we generally recognize revenue ratably over the term of the sponsorship arrangement as the sponsored advertisements are played.

Legacy and other business revenue

For the three months ended December 31, 2023, and 2022, legacy and other business revenue accounts for the remaining

| o | Delivery of streaming services including content encoding and hosting. We recognize revenue over the term of the service based on bandwidth usage. Revenue from streaming services is insignificant. |

| o | Delivery of subscription content services in customized formats. We recognize revenue straight-line over the term of the service. |

| o | Delivery of hardware for ongoing subscription content delivery through software. We recognize revenue at the point of hardware delivery. Revenue from hardware sales is insignificant. |

Transaction prices for performance obligations are explicitly outlined in relevant agreements; therefore, we do not believe that significant judgments are required with respect to the determination of the transaction price, including any variable consideration identified.

Customer acquisition costs

Customer acquisition costs consist of marketing costs and affiliate fees associated with the O&O Platform business. They are included in operating expenses and expensed as incurred.

Cost of revenue

Cost of revenue for the O&O Platform and legacy businesses represents the amortized cost of ongoing licensing and hosting fees, which is recognized over time based on usage patterns. The depreciation expense associated with the Loop Players is not included in cost of sales.

Cost of revenue for the Partner Platform business represents hosting fees, amortized costs of internally-developed content, and the revenue share with third party partners (after deduction of allocated infrastructure costs). The cost of revenue is higher with partners within the Partner Platform versus those within the O&O Platform because we leverage our Partner Platform partners’ network of customers and their screens to deliver content and advertising inventory, rather than using our own Loop Players.

Deferred income

Deferred income represents our accounting for the timing difference between when fees are received and when the performance obligation is satisfied.

12

Net loss per share

We account for net loss per share in accordance with ASC subtopic 260-10, Earnings Per Share (“ASC 260-10”), which requires presentation of basic and diluted earnings per share (“EPS”) on the face of the statement of operations for all entities with complex capital structures and requires a reconciliation of the numerator and denominator of the basic EPS computation to the numerator and denominator of the diluted EPS.

Basic net loss per share is computed by dividing net loss attributable to common stockholders by the weighted average number of shares of Common Stock outstanding during each period. It excludes the dilutive effects of any potentially issuable common shares.

Diluted net loss per share is calculated by including any potentially dilutive share issuances in the denominator.

The following securities are excluded from the calculation of weighted average diluted shares at December 31, 2023, and September 30, 2023, respectively, because their inclusion would have been anti-dilutive.

| December 31, | September 30, | ||

2023 | 2023 | |||

Options to purchase common stock |

| |

| |

Warrants to purchase common stock |

| |

| |

Restricted Stock Units (RSUs) | | | ||

Series A preferred stock |

| — |

| — |

Series B preferred stock |

| — |

| — |

Convertible debentures |

| — |

| — |

Total common stock equivalents |

| |

| |

On December 14, 2023, we entered into Warrant Reprice Letter Agreements with certain holders to amend the exercise price of existing exercisable warrants to $

A reconciliation of the numerator and denominator used in the calculation of basic and diluted net loss per share of our Common Stock is as follows:

Three months ended December 31, | ||||||

2023 | 2022 | |||||

Numerator: | ||||||

Net loss | $ | ( | $ | ( | ||

Plus: Deemed dividend on warrants | ( | — | ||||

Net loss attributable to common stockholders | $ | ( | $ | ( | ||

Denominator: | ||||||

Weighted average number of common shares outstanding | |

| | |||

| ||||||

Basic and diluted net loss per common share | $ | ( | $ | ( | ||

Shipping and handling costs

Loop Players are provided free to our customers. Loop Media absorbs any associated costs of shipping and handling and records as an operational expense at the time of service.

13

Income taxes

We account for income taxes in accordance with ASC Topic 740, Income Taxes (“ASC 740”). ASC 740 requires a company to use the asset and liability method of accounting for income taxes, whereby deferred tax assets are recognized for deductible temporary differences, and deferred tax liabilities are recognized for taxable temporary differences. Temporary differences are the differences between the reported amounts of assets and liabilities and their tax bases. Deferred tax assets are reduced by a valuation allowance when, in the opinion of management, it is more likely than not that some portion, or all of, the deferred tax assets will not be realized. Deferred tax assets and liabilities are adjusted for the effect of changes in tax laws and rates on the date of enactment.

Under ASC 740, a tax position is recognized as a benefit only if it is “more likely than not” that the tax position would be sustained in a tax examination, with a tax examination being presumed to occur. The amount recognized is the largest amount of tax benefit that is greater than 50% likely of being realized on examination. For tax positions not meeting the “more likely than not” test, no tax benefit is recorded. We have no material uncertain tax positions for any of the reporting periods presented.

We recognize accrued interest and penalties related to unrecognized tax benefits as part of income tax expense. We have also made a policy election to treat the income tax with respect to global intangible low-tax income as a period expense when incurred.

In December 2019, the FASB issued ASU No. 2019-12, Simplifying the Accounting for Income Taxes, as part of its initiative to reduce complexity in accounting standards. The amendments in the ASU are effective for fiscal years beginning after December 15, 2020, including interim periods therein. The adoption of this standard in the first quarter of 2022 had no impact on our consolidated financial statements.

In December 2023, the FASB issued ASU 2023-09, Income Taxes (Topic 740): Improvements to Income Tax Disclosures (“ASU 2023-09”). ASU 2023-09 is intended to enhance the transparency and decision usefulness of income tax disclosures. The amendments in ASU 2023-09 address investor requests for enhanced income tax information primarily through changes to the rate reconciliation and income taxes paid information. ASU 2023-09 will be effective for us in the annual period beginning October 1, 2025, though early adoption is permitted. We are still evaluating the presentational effect that ASU 2023-09 will have on our consolidated financial statements, but we expect considerable changes to our income tax footnote.

Stock-based compensation

Stock-based compensation issued to employees is measured at the grant date, based on the fair value of the award, and is recognized as an expense over the requisite service period. We measure the fair value of the stock-based compensation issued to non-employees using the stock price observed in the trading market (for stock transactions) or the fair value of the award (for non-stock transactions), which were more reliably determinable measures of fair value than the value of the services being rendered.

Deferred financing costs

Deferred financing costs represent legal, accounting and other direct costs related to our efforts to raise capital through a public or private sale of our Common Stock. Costs related to the public sale of our Common Stock are deferred until the completion of the applicable offering, at which time such costs are reclassified to additional paid-in-capital as a reduction of the proceeds. Costs related to the private sale of our Common Stock are deferred until the completion of the applicable offering, at which time such costs are amortized over the term of the applicable purchase agreement.

14

Employee retention credits

In March 2020, the Coronavirus Aid, Relief, and Economic Security Act was signed into law, providing numerous tax provisions and other stimulus measures, including the Employee Retention Credit (“ERC”): a refundable tax credit against certain employment taxes. The Taxpayer Certainty and Disaster Tax Relief Act of 2020 and the American Rescue Plan Act of 2021 extended and expanded the availability of the ERC. We qualified for the ERC in the third and fourth quarters of 2020 and the first, second and third quarters of 2021. During the three months ended December 31, 2023, we recorded no aggregate benefit in our condensed combined income statement to reflect the ERC.

Reclassifications

Certain prior year amounts have been reclassified to conform to current year presentation. These reclassifications have no effect on the previously reported financial position, results of operations, or cash flows. Previously reported accounts payable and accrued liabilities have now been disaggregated into accounts payable, accrued liabilities, and accrued royalty. Further, stock-based compensation and depreciation and amortization expenses have now been segregated from sales, general and administrative expenses and separately reported within operating expenses.

Restructuring costs

We undertook initiatives in fiscal year 2023 to increase efficiency and cut costs, while still maintaining our focus on, and dedication to, the continued growth of our business. During fiscal year 2023, we made cuts and adjustments across several aspects of our business. We completed a plan to reduce our overall SG&A costs including labor and various other operating costs. Part of this reduction included eliminating some non-revenue generating headcount, while continuing to invest in expansion of our revenue and ad sales team.

Recently adopted accounting pronouncements

In September 2016, the FASB issued ASU 2016-13, Financial Instruments - Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments. This guidance requires the measurement of all expected credit losses for financial assets held at the reporting date based on historical experience, current conditions and reasonable and supportable forecasts. This guidance also requires enhanced disclosures regarding significant estimates and judgments used in estimating credit losses. The new guidance is effective for fiscal years beginning after December 15, 2022. We are currently evaluating the impact of this standard on our condensed consolidated financial statements and related disclosures. We adopted this ASU as of October 1, 2023, and there is no material impact to our financial statements as of December 31, 2023.

Recent accounting pronouncements

In November 2023, the FASB issued ASU 2023-07, Segment Reporting (Topic 280): Improvements to Reportable Segment Disclosures, that would enhance disclosures for significant segment expenses for all public entities required to report segment information in accordance with ASC 280. ASC 280 requires a public entity to report for each reportable segment a measure of segment profit or loss that its chief operating decision maker (“CODM”) uses to assess segment performance and to make decisions about resource allocations. The amendments in ASU 2023-07 improve financial reporting by requiring disclosure of incremental segment information on an annual and interim basis for all public entities to enable investors to develop more useful financial analyses. Currently, Topic 280 requires that a public entity disclose certain information about its reportable segments. For example, a public entity is required to report a measure of segment profit or loss that the CODM uses to assess segment performance and make decisions about allocating resources. ASC 280 also requires other specified segment items and amounts such as depreciation, amortization and depletion expense to be disclosed under certain circumstances. The amendments in ASU 2023-07 do not change or remove those disclosure requirements. The amendments in ASU 2023-07 also do not change how a public entity identifies its operating segments, aggregates those operating segments, or applies the quantitative thresholds to determine its reportable segments. The amendments in ASU 2023-07 are effective for fiscal years beginning after December 15, 2023, and interim periods within fiscal years beginning after December 15, 2024. Early adoption is permitted. A public entity should apply the

15

amendments in ASU 2023-07 retrospectively to all prior periods presented in the financial statements. We are currently evaluating the impact of this standard on our condensed consolidated financial statements and related disclosures.

In December 2023, the FASB issued ASU 2023-09, Income Taxes (Topic 740): Improvements to Income Tax Disclosures (“ASU 2023-09”). ASU 2023-09 is intended to enhance the transparency and decision usefulness of income tax disclosures. The amendments in ASU 2023-09 address investor requests for enhanced income tax information primarily through changes to the rate reconciliation and income taxes paid information. ASU 2023-09 will be effective for us in the annual period beginning October 1, 2025, though early adoption is permitted. We are still evaluating the presentational effect that ASU 2023-09 will have on our consolidated financial statements, but we expect considerable changes to our income tax footnote.

NOTE 3 – CONTENT ASSETS

Content Assets

The content we stream to our users is generally acquired by securing the intellectual property rights to the content through licenses from, and paying royalties or other consideration to, rights holders or their agents. The licensing can be for a fixed fee or can be a revenue sharing arrangement. The licensing arrangements specify the period when the content is available for streaming, the territories, the platforms, the fee structure and other standard content licensing terms defining the rights and/or restrictions for how the licensed content can be used by Loop Media. We also develop original content internally, which is capitalized when the content is ready and available for streaming, and generally amortized over a period of to

As of December 30, 2023, content assets were $

We recorded amortization expense in cost of revenue, in the consolidated statements of operations, related to capitalized content assets:

| December 31, | |||||

2023 | 2022 | |||||

Licensed Content Assets | $ | | $ | | ||

Internally-Developed Assets | | | ||||

Total | $ | | $ | | ||

Our content license contracts are typically to

Remaining in Fiscal Year 2024 | Fiscal Year 2025 | Fiscal Year 2026 | |||||||

Licensed Content Assets | $ | | $ | | $ | | |||

Internally-Developed Assets |

| |

| |

| | |||

Total | $ | | $ | | $ | | |||

License Content Liabilities

As of December 31, 2023, we had $

16

NOTE 4. PROPERTY AND EQUIPMENT

Our property and equipment, net consisted of the following as of December 31, 2023, and September 30, 2023:

| December 31, | September 30, | ||||

2023 | 2023 | |||||

Loop Players | $ | | $ | | ||

Equipment | | | ||||

Software |

| |

| | ||

| |

| | |||

Less: accumulated depreciation |

| ( |

| ( | ||

Total property and equipment, net | $ | | $ | | ||

For the three months ended December 31, 2023, and 2022, depreciation expense, calculated using straight line method, charged to operations amounted to $

NOTE 5. INTANGIBLE ASSETS

Our intangible assets, each definite lived assets, consisted of the following as of December 31, 2023, and September 30, 2023:

December 31, | September 30, | |||||||

| Useful life |

| 2023 |

| 2023 | |||

Customer relationships | $ | | $ | | ||||

Content library |

| |

| | ||||

Total intangible assets, gross |

| |

| | ||||

Less: accumulated amortization |

| ( |

| ( | ||||

Total |

| ( |

| ( | ||||

Total intangible assets, net | $ | | $ | | ||||

Amortization expense charged to operations amounted to $

Annual amortization expense for the next five years and thereafter is estimated to be $

NOTE 6 – OPERATING LEASES

Operating leases

As of December 31, 2023, we no longer have operating leases for office space and office equipment in excess of

We had

17

We recorded lease expense in sales, general and administration expenses in the consolidated statement of operations:

Three months ended December 31, | ||||||

| 2023 |

| 2022 | |||

Operating lease expense | $ | — | $ | | ||

Short-term lease expense |

| |

| | ||

Total lease expense | $ | | $ | | ||

For the three months ended December 31, 2023, there were

For the three months ended December 31, 2022, cash payments against lease liabilities totaled $

NOTE 7 – ACCOUNTS PAYABLE AND ACCRUED EXPENSES

Accounts payable and accrued expenses consisted of the following as of December 31, 2023, and September 30, 2023:

| December 31, | September 30, | ||||

2023 | 2023 | |||||

Accounts payable | $ | | $ | | ||

Performance bonuses |

| | | |||

Interest payable |

| |

| | ||

Professional fees | | | ||||

Marketing | | | ||||

Commissions | |

| — | |||

Insurance liabilities | | | ||||

Other accrued liabilities | | | ||||

Accrued liabilities |

| |

| | ||

Accrued royalties and revenue share | | | ||||

Total accounts payable and accrued expenses | $ | | $ | | ||

18

NOTE 8 – DEBT

Lines of Credit as of December 31, 2023: | |||||||||||||||

Unpaid | Contractual | ||||||||||||||

Net Carrying Value | Principal | Interest Rates | Contractual | Warrants | |||||||||||

Related party lines of credit: | Current | Long Term | Balance | Cash | Maturity Date | issued | |||||||||

$ | $ | — | $ | — | $ | — | 12 months prior written notice | | |||||||

Total related party lines of credit, net | $ | — | $ | — | $ | — | |||||||||

Lines of credit: | |||||||||||||||

$ | $ | | $ | — | $ | | | ||||||||

$ | | — | | Greater of | — | ||||||||||

$ | — | | | | |||||||||||

Total lines of credit, net | $ | | $ | | $ | | |||||||||

Lines of Credit as of September 30, 2023: | |||||||||||||||

Unpaid | Contractual | ||||||||||||||

Net Carrying Value | Principal | Interest Rates | Contractual | Warrants | |||||||||||

Related party lines of credit: | Current | Long Term | Balance | Cash | Maturity Date | issued | |||||||||

$ | $ | — | $ | | $ | | | ||||||||

Total related party lines of credit, net | $ | — | $ | | $ | | |||||||||

Lines of credit: | |||||||||||||||

$ | $ | | $ | — | $ | | | ||||||||

$ | | — | | Greater of | — | ||||||||||

$ | — | | | | |||||||||||

Total lines of credit, net | $ | | $ | | $ | | |||||||||

19

The following table presents the interest expense related to the contractual interest coupon and the amortization of debt discounts on the lines of credit:

Three months ended December 31, | |||||

2023 | 2022 | ||||

Interest expense | $ | | $ | | |

Amortization of debt discounts | | | |||

Total | $ | | $ | | |

Maturity analysis under the line of credit agreements for the fiscal years ended December 31, | |||

2024 | $ | | |

2025 | | ||

2026 | — | ||

2027 | — | ||

2028 |

| — | |

Lines of credit, related and non-related party |

| ||

Less: Debt discount on lines of credit payable |

| ( | |

Total Lines of credit payable, related and non-related party, net | $ | |

Revolving Lines of Credit

Excel Revolving Line of Credit

Effective as of December 14, 2023, we entered into a Revolving Line of Credit Loan Agreement with Excel Family Partners, LLLP (“Excel” and the “Excel Revolving Line of Credit Agreement”) for up to a principal sum of $

20

Under the terms of the Excel Revolving Line of Credit Agreement, on December 14, 2023, we issued to Excel a warrant to purchase up to an aggregate of

We had not drawn down any funds from the Excel Revolving Line of Credit as of December 31, 2023.

GemCap Revolving Line of Credit Agreement

Effective as of July 29, 2022, we entered into a Loan and Security Agreement with Industrial Funding Group, Inc. (the “Initial Lender”) for a revolving loan credit facility for the initial principal sum of up to $

Under the GemCap Revolving Line of Credit Agreement, we have granted to the Senior Lender a first-priority security interest in all of our present and future property and assets, including products and proceeds thereof. In connection with the loan, our existing secured lenders, some of whom are the RAT Lenders under our RAT Non-Revolving Line of Credit (each as defined below) (collectively, the “Subordinated Lenders”) delivered subordination agreements (the “GemCap Subordination Agreements”) to the Senior Lender. We are permitted to make regularly scheduled payments, including payments upon maturity, to such subordinated lenders and potentially other payments subject to a measure of cash flow and receiving certain financing activity proceeds, in accordance with the terms of the GemCap Subordination Agreements. In connection with the delivery of the GemCap Subordination Agreements by the Subordinated Lenders, on July 29, 2022, we issued warrants to each Subordinated Lender on identical terms for an aggregate of up to

21

The GemCap Revolving Line of Credit had a balance, including accrued interest, amounting to $

Non-Revolving Lines of Credit

RAT Non-Revolving Line of Credit

Effective as of May 13, 2022, we entered into a Secured Non-Revolving Line of Credit Loan Agreement (the “RAT Non-Revolving Line of Credit Agreement”) with several institutions and individuals (each a “RAT Lender” and collectively, the “RAT Lenders”) and RAT Investment Holdings, LP, as administrator of the loan (the “Loan Administrator”) for an aggregate principal amount of $

In connection with the RAT Non-Revolving Line of Credit Agreement, on May 13, 2022, we issued a warrant (collectively, the “RAT Loan Warrants”) to each RAT Lender for an aggregate of up to

Effective as of November 13, 2023, we entered into a Non-Revolving Line of Credit Loan Agreement Amendment (the “RAT Non-Revolving Line of Credit Agreement Amendment”) with the RAT Lenders to: (i) extend the maturity date from eighteen (

22

The RAT Non-Revolving Line of Credit had a balance, including accrued interest, amounting to $

May 2023 Secured Loan

Effective as of May 10, 2023, we entered into a Secured Non-Revolving Line of Credit Loan Agreement (the “May 2023 Secured Line of Credit Agreement”) with several individuals and institutional lenders for aggregate loans of up to $

In connection with the May 2023 Secured Line of Credit, on May 10, 2023, we agreed to issue to each lender under the May 2023 Secured Line of Credit Agreement, upon drawdown, a warrant to purchase up to an aggregate of

As of May 10, 2023, Excel, an entity managed by Mr. Cassidy, had committed to be a lender under the May 2023 Secured Line of Credit Agreement for an aggregate loan of $

As of December 14, 2023, the outstanding principal and interest on Excel’s portion of the May 2023 Secured Line of Credit was $

On December 31, 2023, one of the remaining lenders under the May 2023 Secured Line of Credit converted $

23

The May 2023 Secured Loan had a principal balance, including accrued interest, amounting to $

Excel $2.2M Line of Credit

On May 31, 2023, we entered into a Secured Non-Revolving Line of Credit Loan Agreement (“Excel $2.2M Secured Line of Credit Agreement”) with Excel, an entity managed by Bruce Cassidy, Chairman of our Board of Directors, for an aggregate principal amount of up to $

Under the Excel $2.2M Secured Line of Credit Agreement, we granted to Excel a security interest in all of our present and future assets and properties, real or personal, tangible or intangible, wherever located, including products and proceeds thereof, which security interest was pari passu with the RAT Non-Revolving Line of Credit Agreement, but subordinate in rights to GemCap under the GemCap Revolving Line of Credit Agreement.

On September 12, 2023, we entered into a Pay Off Letter Agreement with Excel, pursuant to which we agreed to pay off the principal and interest outstanding under the $2.2M Line of Credit, amounting to $

The Excel $2.2M Line of Credit had a balance, including accrued interest, amounting to $

See Note 12 – Stock Options, Restricted Stock Units (RSUs) and Warrants for discussion on the repricing and exercise of certain existing warrants.

24

NOTE 9 – COMMITMENTS AND CONTINGENCIES

We may be involved in legal proceedings, claims and assessments arising in the ordinary course of business. Such matters are subject to many uncertainties, and outcomes are not predictable with assurance. There are

NOTE 10 – RELATED PARTY TRANSACTIONS

Related parties are natural persons or other entities that have the ability, directly or indirectly, to control another party or exercise significant influence over the party making financial and operating decisions. Related parties include other parties that are subject to common control or that are subject to common significant influences.

500 Limited

For the three months ended December 31, 2023, and 2022, we paid 500 Limited $

See Note 8 – Debt for discussion on the following:

| ● | GemCap Revolving Line of Credit Agreement and Warrants |

| ● | Excel Revolving Line of Credit |

| ● | May 2023 Secured Loan |

| ● | Excel $ |

See Note 12 – Stock Options, Restricted Stock Units (RSUs) and Warrants for discussion on the repricing and exercise of certain existing warrants.

NOTE 11 –STOCKHOLDERS’ EQUITY (DEFICIT)

Change in Number of Authorized and Outstanding Shares

On August 15, 2023, the Loop stockholders voted at our 2023 Annual Meeting of Stockholders to approve an amendment to our Restated Articles of Incorporation to increase the number of shares of common stock, par value of $

On September 21, 2022, a

Common Stock

Our authorized capital stock consists of

As of December 31, 2023, and 2022, there were

25

Three months ended December 31, 2023

During the three months ended December 31, 2023, we issued

During the three months ended December 31, 2023, we issued

During the three months ended December 31, 2023, we issued

During the three months ended December 31, 2023, we issued

During the three months ended December 31, 2023, we issued

See Note 12 – Stock Options and Warrants for stock compensation discussion.

Three months ended December 31, 2022

See Note 12 – Stock Options and Warrants for stock compensation discussion.

NOTE 12 – STOCK OPTIONS, RESTRICTED STOCK UNITS (RSUs) AND WARRANTS

Options

Option valuation models require the input of highly subjective assumptions. The fair value of stock-based payment awards was estimated using the Black-Scholes option model with a volatility figure derived from using our historical stock prices. We account for the expected life of options based on the contractual life of options for non-employees. For employees, we account for the expected life of options in accordance with the “simplified” method, which is used for “plain-vanilla” options, as defined in the accounting standards codification. The risk-free interest rate was determined from the implied yields of U.S. Treasury zero-coupon bonds with a remaining life consistent with the expected term of the options.

The following table summarizes the stock option activity for the three months ended December 31, 2023:

Number of | Weighted Average | Weighted Average | Aggregate | |||||||

| Options |

| Exercise Price |

| Remaining Contractual Term |

| Intrinsic Value | |||

Outstanding at September 30, 2023 |

| | $ | |

| $ | — | |||

Grants |

| | |

| | |||||

Exercised |

| — |

| — |

|

| ||||

Expired |

| ( |

| |

|

| ||||

Forfeited |

| — |

| — |

|

| ||||

Outstanding at December 31, 2023 |

| | $ | |

| $ | | |||

Exercisable at December 31, 2023 |

| | $ | |

| $ | — | |||

The aggregate intrinsic value in the preceding tables represents the total pretax intrinsic value, based on options with an exercise price less than our stock price of $

We recognize compensation expense for all stock options granted using the fair value-based method of accounting. During the three months ended December 31, 2023, we issued

26

of December 31, 2023, the total compensation cost related to nonvested awards not yet recognized is $

We calculated the fair value of options issued using the Black-Scholes option pricing model, with the following assumptions:

| December 31, 2023 |

| ||

Weighted average fair value of options granted | $ | |||

Expected life |

| | years | |

Risk-free interest rate |

| % | ||

Expected volatility |

| % | ||

Expected dividends yield |

| — | % | |

Forfeiture rate |

| — | % | |

The stock-based compensation expense related to option grants was $

Restricted Stock Units

On September 18, 2022, the Compensation Committee of our Board of Directors approved Restricted Stock Unit (“RSU”) awards to certain officers and key employees pursuant to the terms of the Loop Media, Inc. Amended and Restated 2020 Equity Incentive Compensation Plan (the “2020 Plan”).

On September 22, 2022, we granted an aggregate of

On January 3, 2023, the Compensation Committee of our Board of Directors approved RSU awards as compensation to members of our Board of Directors pursuant to the 2020 Plan.

On January 3, 2023, we granted an aggregate of

On July 1, 2023, we granted an aggregate of

The following table summarizes the RSU activity for the three months ended December 31, 2023:

Number of | Weighted Average | Aggregate | ||||||

RSUs |

| Fair Value |

| Intrinsic Value | ||||

Outstanding at September 30, 2023 | | $ | |

| $ | | ||

Granted | — |

|

| |||||

Vested | ( |

|

|

| ||||

Expired | — |

|

|

| ||||

Forfeited | — |

|

|

| ||||

Outstanding at December 31, 2023 | | $ | |

| $ | | ||

27

The aggregate intrinsic value in the preceding tables represents the total pretax intrinsic value, based on our stock price of $

The stock-based compensation expense related to RSU grants was $

As of December 31, 2023, the total compensation cost related to nonvested RSU awards not yet recognized was $

Warrants

The following table summarizes the warrant activity for the three months ended December 31, 2023:

Number of | Weighted average exercise | ||||

shares | price per share | ||||

Outstanding at September 30, 2023 | | $ | | ||

Issued | | ||||

Exercised | ( | ||||

Expired | — | ||||

Outstanding at December 31, 2023 |

| | $ | | |

We record all warrants granted using the fair value-based method of accounting.

During the three months ended December 31, 2023, we issued

During the three months ended December 31, 2023, we recorded consulting expense of $

We calculated the fair value of warrants issued using the Black-Scholes option pricing model, with the following assumptions:

| December 31, 2023 | |||

Weighted average fair value of warrants granted | $ | | ||

Expected life |

| .00 | years | |

Risk-free interest rate |

| | % | |

Expected volatility |

| | % | |

Expected dividends yield |

| — | % | |

Forfeiture rate |

| — | % | |

Repricing and Exercise of Certain Existing Warrants

On December 14, 2023, we agreed to offer to amend certain existing warrants exercisable for an aggregate of up to

28

Price of each respective Existing Warrant in cash to the Company (the “Warrant Repricing”). Holders of Existing Warrants had until 4:00 p.m., Eastern Time, on December 31, 2023, to enter into a Warrant Reprice Letter Agreement, after which time the original per share warrant exercise price of Existing Warrants would remain unchanged. Existing Warrants exercisable for an aggregate of up to

NOTE 13 – SUBSEQUENT EVENTS

We have evaluated all subsequent events through the date of this quarterly report on Form 10-Q with the SEC, to ensure that this filing includes appropriate disclosure of events both recognized in the financial statements as of December 31, 2023, and events that occurred after December 31, 2023, but which were not recognized in the financial statements.

On January 8, 2024, we filed a Prospectus Supplement to the Prospectus filed on January 11, 2023, to decrease the amount of our Common Stock that is available to be sold under the ATM Sales Agreement, such that we registered the offer and sale of our Common Stock having an aggregate sales price of up to $

Item 2.Management’s Discussion and Analysis of Financial Condition and Results of Operations.

STATEMENT ON FORWARD-LOOKING INFORMATION

This report (“Report”) on Form 10-Q contains certain forward-looking statements. All statements other than statements of historical fact are “forward-looking statements” for purposes of these provisions, including any projections of earnings, revenues, or other financial items; any statements of the plans, strategies, and objectives of management for future operations; any statements concerning proposed new products, services, or developments; any statements regarding future economic conditions or performance; statements of belief; and any statement of assumptions underlying any of the foregoing. Such forward-looking statements are subject to inherent risks and uncertainties, and actual results could differ materially from those anticipated by the forward-looking statements.

These forward-looking statements involve significant risks and uncertainties, including, but not limited to, the following: competition, promotional costs and risk of declining revenues. Our actual results could differ materially from those anticipated in such forward-looking statements as a result of a number of factors. These forward-looking statements are made as of the date of this filing, and we assume no obligation to update such forward-looking statements. The following discusses our financial condition and results of operations based upon our financial statements which have been prepared in conformity with accounting principles generally accepted in the United States of America. It should be read in conjunction with our financial statements and the notes thereto included elsewhere herein.

The following discussion and analysis provides information which our management believes to be relevant to an assessment and understanding of our results of operations and financial condition. The discussion should be read together with our financial statements and the notes to the financial statements, which are included in this Report.

Overview

We are a multichannel digital video platform media company that uses marketing technology, or “MarTech,” to generate our revenue and offer our services. Our technology and vast library of videos and licensed content enable us to curate and distribute short-form videos to connected televisions (“CTV”) in out-of-home (“OOH”) dining, hospitality and retail establishments, convenience stores and other locations and venues to enable the operators of those locations to inform, entertain and engage their customers. Our technology also provides businesses the ability to promote and advertise

29

their products via digital signage and provides third-party advertisers with a targeted marketing and promotional tool for their products and services. We also allow our business clients to access our service without advertisements by paying a monthly subscription fee.

We offer hand-curated music video content licensed from major and independent record labels, including Universal Music Group (“Universal”), Sony Music Entertainment (“Sony”), and Warner Music Group (“Warner” and collectively with Universal and Sony, the “Music Labels”), as well as non-music video content. Our non-music video content is predominantly licensed or acquired from third parties, including action sports clips, drone and nature footage, trivia, news headlines, lifestyle channels and kid-friendly videos, as well as movie, television and video game trailers, amongst other content. We distribute our content and advertising inventory to digital screens located in OOH locations primarily through (i) our owned and operated platform (the “O&O Platform”) of Loop Media-designed “small-box” streaming Android media players (“Loop Players”) and legacy ScreenPlay (as defined below) computers and (ii) through screens (“Partner Screens”) on digital platforms owned and operated by third parties (each a “Partner Platform” and collectively the “Partner Platforms,” and together with the O&O Platform, the “Loop Platform”).

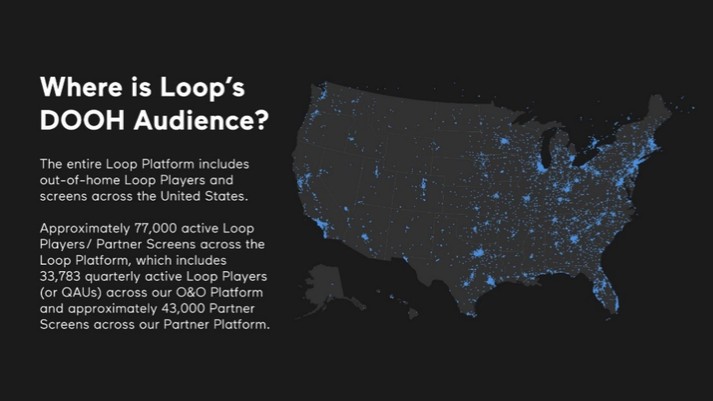

As of December 31, 2023, we had approximately 77,000 active Loop Players and Partner Screens across the Loop Platform, which include 33,783 quarterly active Loop Players, or QAUs (as defined below) across our O&O Platform, an increase of 26% (or 6,880 QAUs) over the 26,903 QAUs for the quarter ended December 31, 2022, and a decrease of 3,238 over the 37,021 QAUs for the quarter ended September 30, 2023, and approximately 43,000 Partner Screens across our Partner Platforms, an increase of 153% (or 26,000) over the 17,000 Partner Screens for the quarter ended December 31, 2022, and an increase of 1,000 Partner Screens over the 42,000 Partner Screens for quarter ended September 30, 2023. See “— Key Performance Indicators.”

We have two primary constituents that are included in our customer base: the OOH locations we service and the advertisers who purchase advertising inventory on the Loop Platform. We earn revenue from these customers primarily by selling advertising inventory on the Loop Platform and by collecting subscription fees from our O&O Platform owners and operators that are streaming advertising-free content.

The O&O Platform

The foundation of our business model is built around the OOH experience, with a focus on distributing licensed music videos and other content to public-facing business venues and locations. Our OOH offering has supported hospitality and retail businesses for over 20 years, originally through ScreenPlay, Inc. (“ScreenPlay”), which we fully acquired in 2019. Since the acquisition of ScreenPlay, we have primarily focused on acquiring OOH clients throughout the United States. We have sought very limited expansion into Canada and are testing potential expansion into New Zealand and Australia.

We deliver content across our O&O Platform to the owners and operators of OOH locations who sign up for our media service. We sell advertising impressions contained in the content streams to demand sources, including demand-side platforms (“DSPs”), supply-side platforms (“SSPs”) and advertisers, who pay us to fill those impressions and have their ads delivered into the OOH locations that utilize our services. We also allow OOH locations on our O&O Platform to access our content without advertisements by paying a monthly subscription fee.

From a business operations standpoint, for the O&O Platform business, we view our customers as the owners and operators of the OOH locations that use our content services to engage and entertain the customers that visit the OOH locations. Our customer services team works with the owners and operators of OOH locations in our O&O Platform business to ensure our customers are being properly serviced and addressing any questions about the service, content, advertising performance and other matters.

From an accounting standpoint, for the O&O Platform business, our customers are considered to be those persons that provide revenue to us, which includes the owners and operators of the OOH locations that utilize a subscription-based service, and the advertising demand sources (including DSPs, SSPs and advertisers) that purchase our advertising inventory on the O&O Platform. From an accounting standpoint, the owners and operators of the OOH

30

locations utilizing a free advertising-based service on our O&O Platform are not our customers. Instead, it is the advertising demand sources that are our customers because they are providing revenue to us (by way of purchasing advertising inventory) for the streaming of content to those OOH locations utilizing an ad-free service.

We record as cost of revenue in the O&O Platform business certain costs and expenses associated with operating such business, including the cost of content, streaming costs, and content hosting fees. We procure content from third parties though licensing fees or by purchasing the content outright. Certain of our content, including our music video and certain third-party non-music content, are under licenses that contain a revenue share arrangement. We and the licensor of the content negotiate and pre-agree the percentage of revenue to which each party is entitled. The cost of content, including any payments to licenses under a revenue share license, is the single largest component of the cost of revenue associated with the O&O Platform business.

The Partner Platform

The screens in our Partner Platform business may deliver content that we curate and deliver or content that is provided by the owners and operators of third-party digital platforms. We make available to our Partner Platforms clients’ channels of original content developed using licensed or purchased content that is then reformatted into short-form content suitable for commercial use.

We provide advertising demand services to third parties by selling ad impressions available on the Partner Platform to advertising demand sources (including DSPs, SSPs and advertisers) who pay us to fill those impressions and have ads delivered across the Partner Platform. If the advertising impressions are filled with advertisements, we will fulfill our obligation and be paid as the publisher of the advertisement. If advertising impressions are not purchased, the content will play without advertisements and no revenue will be earned by us.

From a business operations standpoint, for our Partner Platform services, we view as our customers the owners and operators of the third-party digital platforms that utilize our content and advertising services and enable such third parties to better monetize the screens on their digital platforms. We may, in certain instances, also provide content across the Partner Platform.

Our customer services team works with the owners and operators of the third-party digital platforms in our Partner Platform business to ensure our customers are being properly serviced and addressing any questions about the service, content, advertising performance and other matters.

From an accounting standpoint, for the Partner Platform business, our customers are the advertising demand sources (including DSPs, SSPs and advertisers) because they are providing revenue to us (by way of purchasing advertising inventory) for the streaming of content across the Partner Platform. The Partner Platform business operates a free-ad supported business model and has no subscription fees.

The revenue share arrangements in the O&O Platform business are included in the cost of revenue. The content streamed on the Partner Platforms is content we procure on licenses that do not contain an element of revenue share or content provided by the third-party partner who owns and operates the screens on the Partner Platform. As such, there are no content partner revenue share arrangements on the Partner Platform. There is, however, a revenue share arrangement with the third-party partner who owns and operates the screens on the Partner Platform. We deduct from the revenue we generate in the Partner Platform business certain costs and expenses associated with operating such business (including streaming costs and content hosting) and then allocate the remaining revenue between us and the third-party digital platform provider, based on pre-agreed negotiated percentages. The percentage of revenue we pass along to third-party digital platform providers is recorded as cost of revenue and is our single largest cost of revenue component for the Partner Platform business.

31

Key Performance Indicators

We review our quarterly active units (“QAUs”) and average revenue per unit player (“ARPU”), among other key performance indicators, to evaluate our business, measure our performance, identify trends affecting our business, formulate financial projections and make strategic decisions.

Quarterly Active Units

We define an “active unit” as (i) an ad-supported Loop Player DOOH (defined below) location using our ad- supported service through our “Loop for Business” application or using an DOOH venue-owned computer screening our content) that is online, used on our O&O Platform, playing content and has checked into the Loop Media analytics system at least once in the 90-day period ending on the date of measurement, or (ii) a DOOH location customer using our subscription service on our O&O Platform at any time during the 90-day period. We use “QAU” to refer to the number of such active units during such period. We do not count towards our QAUs any Loop Players or screens used on our Partner Platform.

Digital out-of-home (“DOOH”) is a form of media that is delivered digitally outside of the home on billboards, signage, displays, televisions, and other devices in OOH locations, including restaurants, retail shops, healthcare facilities, sports and entertainment venues, and other public or non-residential spaces.